Steve Keen's Macroeconomic Model, Derivation, Code

Based on papers, code seen in the References section below.

Terms

$\alpha$: productivity growth rate, $\frac{d a}{d t} = \alpha a$

$\beta$: population growth rate, $\frac{d N}{d t} = \beta N$

The level of capital stock K determines the level of output per annum $Y$ via the accelerator $K = v \cdot Y$

The level of output determines the level of employment $L$ via labor productivity $a$: $L = Y/a$

$w$: the rate of change of real wages, all wages $W = w \cdot L$.

The employment rate determines the rate of change of real wages

$\dot{w} = \Phi(\lambda) \cdot w$: via Philips curve

$$ \Phi(\lambda) = \frac{\phi_1}{(1-\lambda)^2}-\phi_0 $$

$\omega$: the wage share of the economy $\omega=\frac{w\cdot L}{a \cdot L} = \frac{w}{a}$

$\Pi = (1-\omega-rd)Y$, Profit share is a residual after workers and debt repayment (to bankers)

Profit determines investment I, all profits are invested, $I=\Pi$.

Investment minus depreciation determines the rate of change of capital stock $K$. So $\dot{K} = I - \delta K =\kappa(1 - \omega - rd) Y - \delta K$:

$\delta K$. $\kappa(x)$ is a nonlinear function such as $\kappa(x) = \kappa_0 + \kappa_1 \exp(\kappa_2 x)$.

$\frac{d D}{d t} = \dot{D} = I - \Pi$: the rate of change of debt D is investment minus profits (where profits are now net of interest payments, which equal the interest rate r times the debt level.

Core Definitions

1) The employment rate: the number of people with a job (L) divided by the total population (N). $\lambda = L/N$.

2) The wages share of output: the total wage bill (W) divided by GDP (Y). $\omega = W/Y$.

3) The private debt to GDP ratio: Private Debt (D) divided by GDP (Y). $d = D/Y$.

Differentiate them with respect to time. Since the definitions are true by definition, so are these dynamic re-statements of them:

1) The (percentage) employment rate will grow if the (percentage) rate of real (inflation-adjusted) economic growth exceeds the sum of the rate of population growth plus the rate of growth of labour productivity (after log differentiation)

$$\frac{\dot{\omega}}{\omega} = \frac{\dot{W}}{W} - \frac{\dot{Y}}{Y}$$

2) The wages share of output will grow if wage growth exceeds the growth in labour productivity; and

$$\frac{\dot{d}}{d} = \frac{\dot{D}}{D} - \frac{\dot{Y}}{Y}$$

3) The private debt to GDP ratio will rise if debt rises faster than the rate of economic growth.

$$\frac{\dot{\lambda}}{\lambda} = \frac{\dot{L}}{L} - \frac{\dot{N}}{N}$$

Note:

Log differentiation is used a lot, which in general form is,

$$f(x) = \frac{g(x)}{h(x)}$$

$$ \ln (f(x)) = \ln \bigg( \frac{g(x)}{h(x)} \bigg) = \ln(g(x)) - \ln(f(x)) $$

$$\frac{f'(x)}{f(x)} = \frac{g'(x)}{g(x)} - \frac{h'(x)}{h(x)}$$

Moving on, trying to reach an ODE

1)

$$= \frac{\dot{w}}{w} + \frac{\dot{L}}{L} - \frac{\dot{Y}}{Y}$$

$$= \frac{\dot{w}}{w} + \frac{\dot{L}}{L} - \frac{\dot{L}}{L} - \alpha$$

$$\frac{\dot{\omega}}{\omega} = \frac{\dot{w}}{w} - \alpha = \Phi(\lambda)-\alpha$$

2)

$$\dot{D} = I - \Pi = \kappa(1 - \omega - rd) Y - (1-\omega-rd)Y$$

3)

$$ \frac{\dot{D}}{D} = \frac{ \kappa(1 - \omega - rd)}{d} - \frac{(1-\omega-rd)}{d} $$

$$ = \frac{ \kappa(1 - \omega - rd) - (1-\omega-rd) }{d} $$

Calculate $\dot{Y}/Y$, bcz $\dot{Y}/Y = \dot{K}/K$

$$ \dot{Y}/Y = \dot{K}/K = \frac{\kappa(1 - \omega - rd) Y - \delta K}{K} $$

$$ = \frac{\kappa(1 - \omega - rd) }{v}- \delta (1) $$

$$ \scriptstyle \frac{\dot{D}}{D} - \frac{\dot{Y}}{Y} = \frac{ \kappa(1 - \omega - rd) - (1-\omega-rd) }{d} - \frac{\kappa(1 - \omega - rd) }{v} + \delta $$

3)

$$ = \frac{\dot{L}}{L} - \frac{\dot{a}}{a} = \frac{\dot{L}}{L} - \beta $$

$$Y = L \cdot a$$

$$ \frac{\dot{Y}}{Y} = \frac{\dot{L}}{L} + \frac{\dot{a}}{a} = \frac{\dot{L}}{L} + \alpha $$

$$ \frac{\dot{\lambda}}{\lambda} = \frac{\dot{Y}}{Y} - \alpha - \beta $$

Use (1) $\dot{Y}/Y$

$$ \frac{\dot{\lambda}}{\lambda} = \frac{\kappa(1-\omega-rd)}{v} - \alpha - \beta - \delta $$

So we reach ODE

$$\dot{\omega} = \omega [ \Phi(\lambda)-\alpha ] (2)$$

$$ \dot{\lambda}= \lambda \bigg[ \frac{\kappa(1-\omega-rd)}{v} - \alpha - \beta - \delta \bigg] (3) $$

$$ \scriptstyle \dot{d} = d \bigg[ r - \frac{\kappa(1-\omega-rd)}{v} + \alpha \bigg] + \kappa(1-\omega-rd) - (1-\omega) (4) $$

Some constants, funcs, will be used later

import numpy as np

import matplotlib.pyplot as plt

alpha = 0.025

beta = 0.02

delta = 0.01

v = 3.0

k0 = -0.0065

k1 = np.exp(-5.0)

k2 = 20.0

r = 0.03

phi0 = 0.04 / (1.0-(0.04**2))

phi1 = 0.04**3.0 / (1.0-(0.04**2))

def kappa(x,k0,k1,k2): return k0 + (k1*np.exp(k2*x))

def philips(lam,phi0,phi1): return ( (phi1 / (1.0-lam)**2) - phi0)

Stable points

(0,0,0) economically meaningless. For meaningful pts for (2) set to zero, $\Phi(\lambda)=\alpha$ or $\lambda=\Phi^{-1}(\alpha)$, we r looking for inverse so that $\Phi^{-1}(\Phi(\lambda)) = \lambda$, then

$$ \Phi(\lambda) = \alpha = \frac{\phi_1}{(1-\lambda)^2}-\phi_0$$

Rearrange

$$ \alpha + \phi_0 = \frac{\phi_1}{(1-\lambda)^2}$$

$$ (1-\lambda)^2 = \frac{\phi_1}{ \alpha + \phi_0} $$

$$ \lambda^2 - 2\lambda + 1 - \frac{\phi_1}{ \alpha + \phi_0} =0$$

Find roots

res = np.roots([1, -2, 1-(phi1/(alpha+phi0))])

lambda1 = res[1]

print (res)

[1.03138824 0.96861176]

Moving on, set (3) to zero, nontrivial sol, start with

$$ \kappa(1-\omega-rd)= v (\alpha + \beta + \delta)$$ (5)

Inverse

$$\overline{\pi}_1 = 1-\omega-rd= \kappa^{-1}(v (\alpha - \beta - \delta))$$

Very useful, bcz $\overline{\pi}_1$ depends only on constants. Let's calculate

tmp = v*(alpha+beta+delta) - k0

pi1 = 1.0/k2 * np.log(np.abs(tmp/k1))

print ('pi1', pi1)

pi1 0.1618413993811929

For $\overline{\omega}_1$ rearran (5)

$$d = \frac{1-\overline{\pi}_1-\omega}{r}$$

Plug into (4),

$$ \scriptstyle 0 = \frac{1-\overline{\pi}_1-\omega}{r} \bigg[ r - \frac{v (\alpha + \beta + \delta)}{v} + \delta \bigg] + v (\alpha + \beta + \delta)- 1+\omega $$

$$ \scriptstyle -\omega = \bigg(\frac{1}{r}-\frac{\overline{\pi}_1}{r}-\frac{\omega}{r}\bigg) \bigg( r - \alpha - \beta \bigg) + v (\alpha + \beta + \delta)- 1 $$

skipping some algebra

$$ \overline{\omega}_1 = \frac{c_1 - c_1\overline{\pi}_1 + rc_2 - r}{c_1 - r} $$

c1 = r-alpha-beta

c2 = v*(alpha+beta+delta)

omega1 = (c1 - c1*pi1+r*c2-r) / (c1-r)

print (omega1)

0.8360528668729358

For $d$ take $\overline{\pi}_1$ formula, plug in known vals

$$ \overline{\pi}_1 = 1-\omega-rd => d = (1-\overline{\omega}_1 -\overline{\pi}_1) / r $$

d1 = (1-omega1-pi1) / r

print (d1)

0.07019112486237693

Fixed point

fp1 = (lambda1,omega1,d1)

print (np.round(fp1,4))

[0.9686 0.8361 0.0702]

Solve ODE

import scipy as sp

from scipy.integrate.odepack import odeint

def rhs(u,t,alpha,beta,delta,r,k0,k1,k2,v,phi0,phi1):

omega, lam, d, a, N = u

tmp = kappa(1.0-omega-r*d,k0,k1,k2)

res = [omega*(philips(lam,phi0,phi1)-alpha), \

lam*(tmp/v - alpha - beta - delta), \

d * ( r - tmp/v + alpha ) + tmp - (1.0-omega), \

alpha*a, \

beta*N]

return res

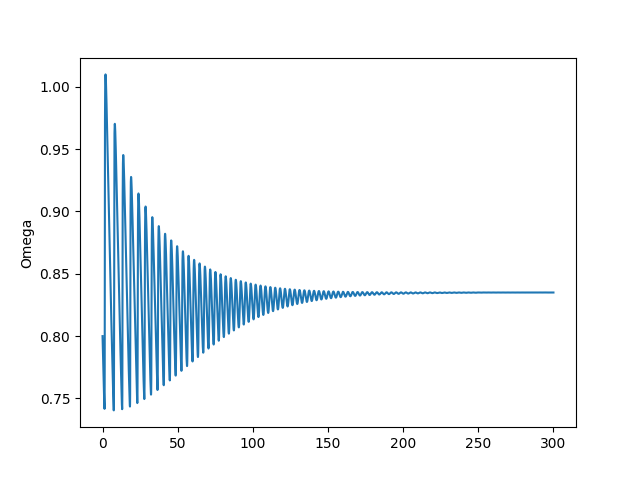

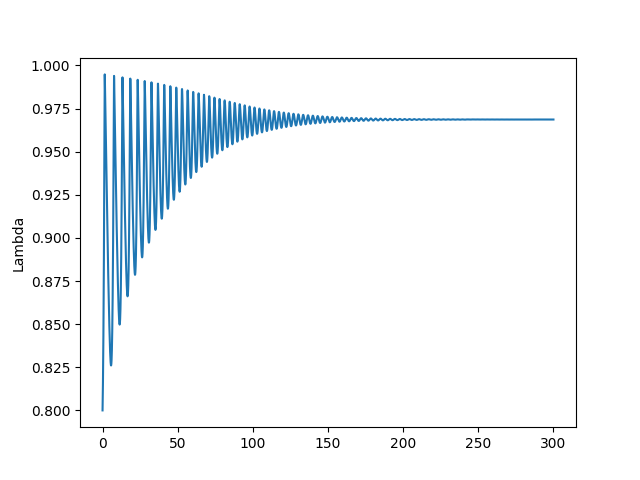

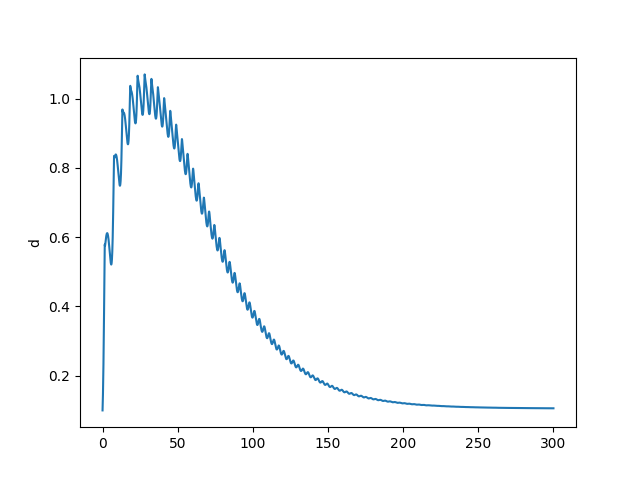

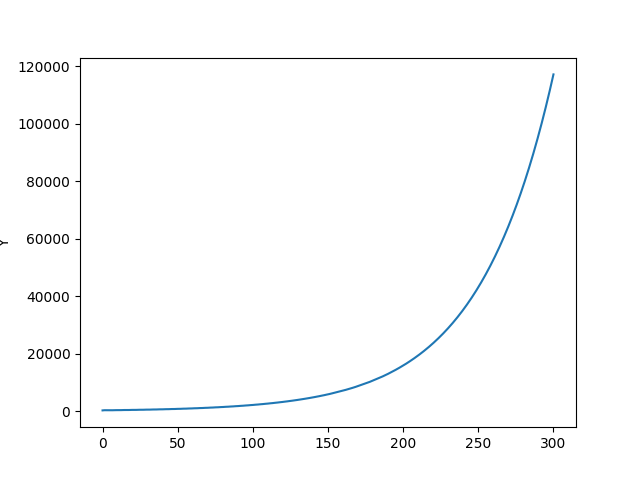

First start from values close to fixed point

omega0 = 0.80

lam0 = 0.80

d0 = 0.1

a0 = 0.5

N0 = 300.

t=np.linspace(0.0,300.0,10000)

args = (alpha,beta,delta,r,k0,k1,k2,v,phi0,phi1)

res=odeint(rhs,[omega0, lam0, d0, a0, N0],t,args=args)

omega1, lam1, d1, a1, N1=res[:, 0],res[:, 1],res[:, 2],res[:, 3],res[:, 4]

Y = lam1*N1

plt.figure()

plt.plot(t,omega1)

plt.ylabel('Omega')

plt.savefig('out_01.png')

plt.figure()

plt.plot(t,lam1)

plt.ylabel('Lambda')

plt.savefig('out_02.png')

plt.figure()

plt.plot(t,d1)

plt.ylabel('d')

plt.savefig('out_03.png')

plt.figure()

plt.plot(t,Y)

plt.ylabel('Y')

plt.savefig('out_04.png')

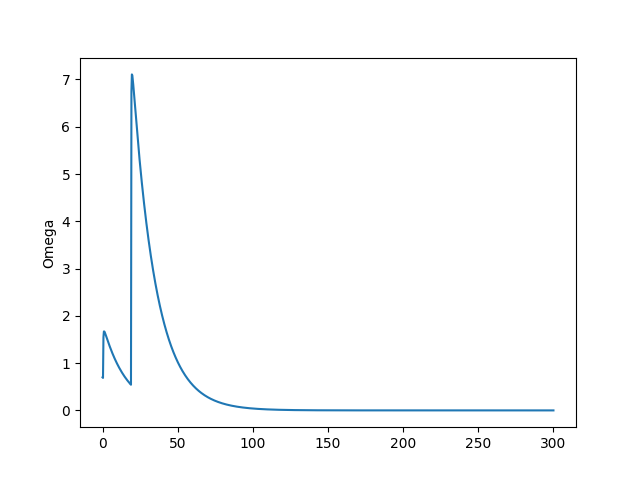

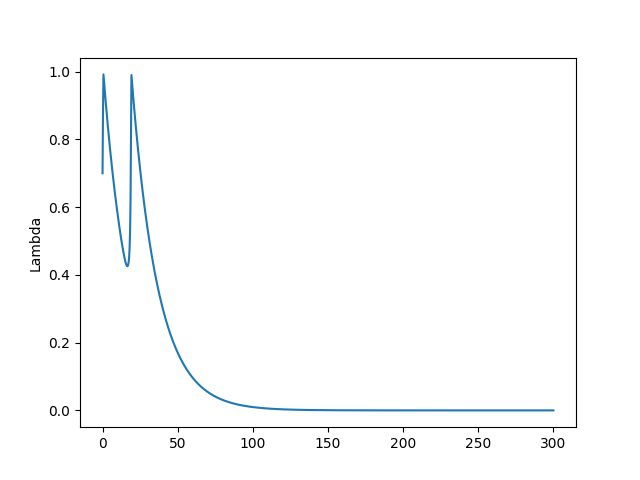

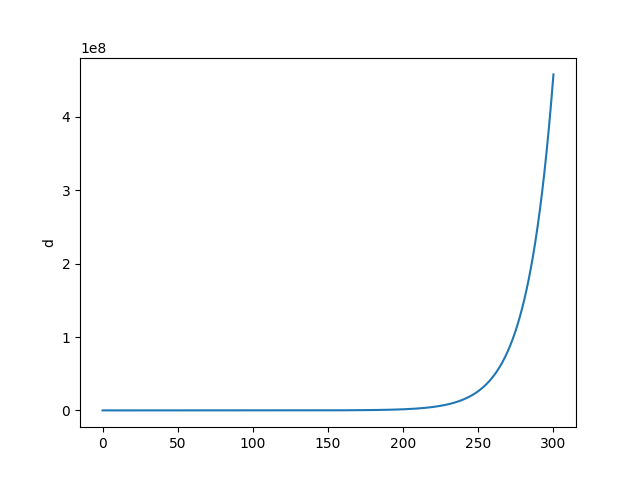

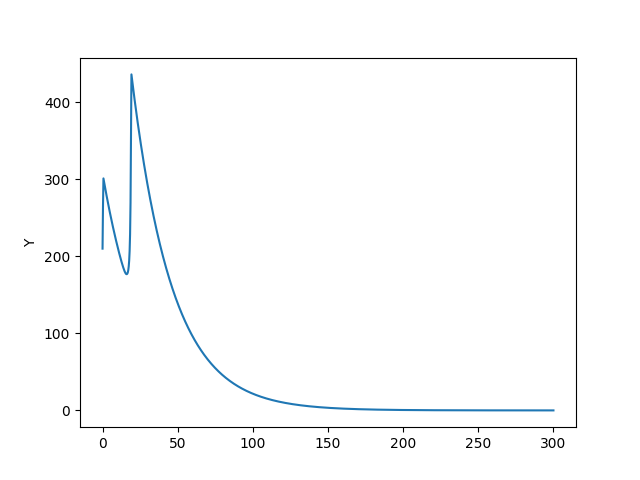

Now try starting little away from the fixed point - graph shows we end up in purgatory.

omega0 = 0.70

lam0 = 0.70

d0 = 0.1

a0 = 0.5

N0 = 300.

t=np.linspace(0.0,300.0,1000)

args = (alpha,beta,delta,r,k0,k1,k2,v,phi0,phi1)

res=odeint(rhs,[omega0, lam0, d0, a0, N0],t,args=args)

omega2, lam2, d2, a2, N2=res[:, 0],res[:, 1],res[:, 2],res[:, 3],res[:, 4]

Y = lam2*N2

plt.figure()

plt.plot(t,omega2)

plt.ylabel('Omega')

plt.savefig('out_05.png')

plt.figure()

plt.plot(t,lam2)

plt.ylabel('Lambda')

plt.savefig('out_06.png')

plt.figure()

plt.plot(t,d2)

plt.ylabel('d')

plt.savefig('out_07.png')

plt.figure()

plt.plot(t,Y)

plt.ylabel('Y')

plt.savefig('out_08.png')

Inflation [3,4]

$g$ is the real growth rate, which is determined by the rate of investment and depreciation, $I_{fn}$ is non-linear investment function,

$$ g = \frac{I_{fn}(\pi_r)}{v} - \delta_{Kr} $$

$$ \frac{\dot{\lambda}}{\lambda} = \left( \underbrace{ g }_{A} - \underbrace{ (\alpha + \beta) }_{B} \right) $$

A: Growth Rate

B: Labor productivity and population growth

"Employment rises if the growth rate exceeds population growth and labor productivity."

$$ \frac{\dot{\omega}}{\omega} = \left( (\underbrace{w_{fn}(\lambda)}_{A} - \underbrace{\alpha}_{B}) + \frac{1}{\tau_p} \underbrace{\left( 1-\frac{1}{1-s} \cdot \omega \right)}_{C} \right) $$

A: Wage share

B: Labor productivity

C: Inflation

"Wage share rises if money wage demands greater than labor productivity and the inflation rate"

$$ \scriptstyle \frac{\dot{d}}{d} = \underbrace{\frac{\left( \frac{I_{fn}(\pi_r)}{v} \right) - \pi_s }{d}}_{A} - \left[ \underbrace{g }_{B}+ \underbrace{\frac{1}{\tau_p} \left(1 - \frac{1}{1-s} \omega\right)}_{C} \right] $$

A: Debt growth rate

B: Real growth rate

C: Inflation

"Debt ratio will rise if debt growth rate is greater than real growth rate plus inlation"

For price level we look into supply/demand in equilibrium. The derivative of $P$ according to time is inflation, change in price level. Production $Q$ equals physical demand $D$. $Q = a \cdot L$, productivity times labor. For $L$ we divide wage money flow with indiv wage.

$$ L = (1-s) \frac{F_D / \tau_s}{W} $$

$F_D/\tau_s$ is GDP, $F_D$ is company's money, $\tau_s$ is the turnover of that money, multiply that by $1-s$ to find worker's share. Divide that by unit wage $W$, we find labor force. Then production is

$$ Q = a \cdot (1-s) \frac{F_D / \tau_s}{W} $$

Physical demand is money flow towards demand divided by price level, expenditure divided by $P$, so $(F_D / \tau_s) / P$. There is no $1-s$ now, labor and corp demand added.

Equate $D$ and $Q$ and solve for $P$,

$$ a \cdot (1-s) \frac{F_D / \tau_s}{W} = \frac{(F_D / \tau_s)}{P} $$

$F_D,\tau_s$ cancels out, rearrange,

$$ P = \frac{1}{1-s} \frac{W}{a}$$

This is price level in equilibrium, we need a dynamic version, first-order approx. converging to RHS above,

$$ \frac{d P}{d t} = \frac{-1}{\tau_p} \left( P - \frac{1}{1-s} \frac{W}{a} \right) $$

$\tau_p$ might be familiar from ODE's, ex,

$$ \frac{d x}{d t} = k(10-x)$$

is solved by $x = 10 - C e^{-kt}$, $k$ controls convergence. $t=0,x=0$ gives $C=10$, $x = 10 (1 - e^{-kt})$. In general

$$ x = x_{max} (1-e^{-t/\tau}) $$

For $t=\tau,x_{max}=1$ we get $1-e^{-1}$

print (1-np.exp(-1))

0.6321205588285577

$\tau$ could be seen as approximately how many time steps it takes to reach 63\% of the target val.

Final equations

$$ \frac{\dot{\lambda}}{\lambda} = g - (\alpha + \beta) $$

$$ \frac{\dot{\omega}}{\omega} = \left( (w_{fn}(\lambda) - \alpha) + \frac{1}{\tau_p} \left( 1-\frac{1}{1-s} \cdot \omega\right) \right) $$

$$ \frac{\dot{d}}{d} = \frac{\left( \frac{I_{fn}(\pi_r)}{v} \right) - \pi_s }{d} - \left[ g + \frac{1}{\tau_p} \left(1 - \frac{1}{1-s} \omega\right) \right] $$

$$ g = \frac{I_{fn}(\pi_r)}{v} - \delta_{Kr} $$

Compute,

import scipy as sp

from scipy.integrate.odepack import odeint

def rhs(u,t,alpha, beta, delta, nu, r_b, s, tau_p, tau_i, x_i, y_i, s_i, m_i, x_w, y_w, s_w, m_w):

lam, omega, d, i = u

r=r_b;

if i>0: r=r+i;

p=1.0-omega-r*d;

f=-(1.0/tau_p)*(1.0-omega/(1.0-s));

I=(y_i-m_i)*np.exp(s_i*((p/nu)-x_i)/(y_i-m_i))+m_i;

W=(y_w-m_w)*np.exp(s_w*(lam-x_w)/(y_w-m_w))+m_w;

return [( ((1.0/nu)*I-delta) -(alpha + beta) )*lam, \

( W - (alpha+f) )*omega, \

( I-p ) -( (1/nu)*I - delta + f )*d,\

-(1.0/tau_i)*(i-f)]

alpha=0.025;

beta=0.015;

delta=0.07;

nu=3.0;

r_b=0.04;

s=0.3;

tau_p=1.0;

tau_i=0.5;

x_i=0.03;

y_i=0.03;

s_i=2.25;

m_i=0;

x_w=0.6;

y_w=0.0;

s_w=1.0;

m_w=-0.04;

# initial values

lambda0=0.65; # employment

omega0=0.82; # wage share of gdp

d0=0.5; # debt

i0=0.1; # inflation

arg0 = (alpha, beta, delta, nu, r_b, s, tau_p, tau_i, x_i, y_i, s_i, m_i, x_w, y_w, s_w, m_w)

T=80.0

t=np.linspace(0.0,T,1000)

res=odeint(rhs,[lambda0, omega0, d0, i0],t,args=arg0)

lambda1,omega1,d1,i1=res[:, 0],res[:, 1],res[:, 2],res[:, 3]

plt.plot(t, 100.0*i1)

plt.xlabel(u'Year')

plt.ylabel(u'Annual Inflation')

plt.savefig('inf_01.png')

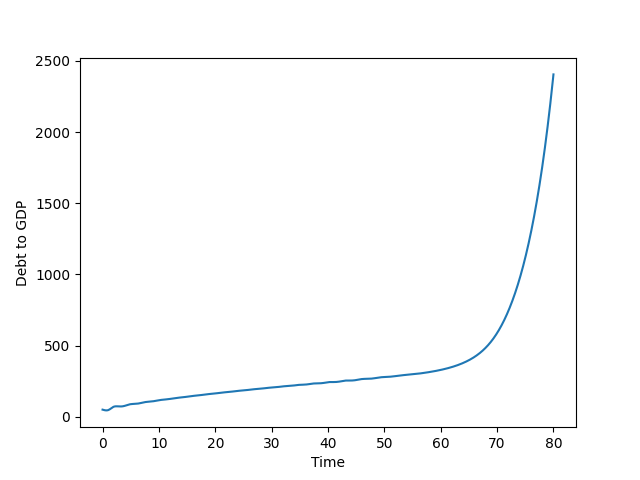

plt.plot(t, 100.0*d1)

plt.xlabel(u'Time')

plt.ylabel(u'Debt to GDP')

plt.savefig('inf_02.png')

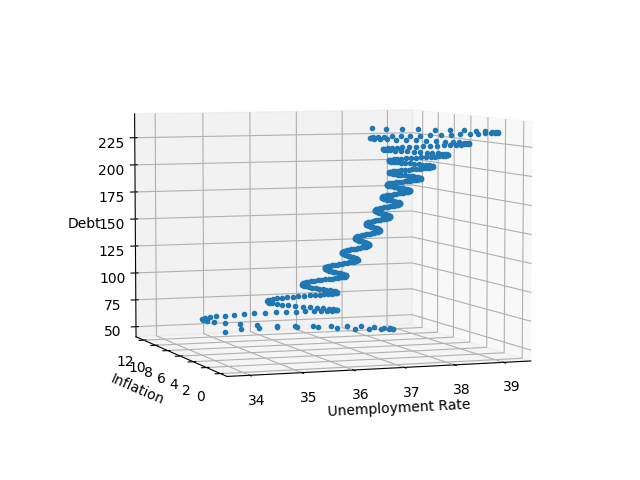

last=500;

x1=100.0*(1.0-lambda1[:last]);

x2=100.0*i1[:last];

x3=100.0*d1[:last];

from mpl_toolkits.mplot3d import Axes3D

from matplotlib import cm

fig = plt.figure()

ax = Axes3D(fig)

ax.plot(x1,x2,x3,'.')

ax.set_xlabel(u'Unemployment Rate')

ax.set_ylabel(u'Inflation')

ax.set_zlabel(u'Debt')

ax.view_init(elev=5, azim=250)

plt.savefig('inf_03.png')

References

[1] Keen, On Macroeconomic modelling, http://www.profstevekeen.com/crisis/models

[2] Grasselli, An analysis of the Keen model for credit expansion, asset price bubbles and financial fragility,

[3] Keen, A monetary Minsky model of the Great Moderation and the Great Recession

[4] Keen, Greenwich-Kingston PhD students lecture: the logic maths of modelling Minsky (2), http://youtu.be/0Do05hV_Iqo?t=1200