Sornette's Model and Code

Main equation

$$ \small{ \ln(p(t)) = A + B(t_c - t)^\beta \big[ 1 + C \cos (\omega \ln(t_c-t) + \phi ) \big] } $$

Simplified form derivation below: start with logistic equation,

$$ \frac{dp}{dt} = rp(t) [ K - p(t) ] $$

$$ \frac{dp}{dt} = r [p(t)]^{1+\delta} $$

$$ \int \frac{dp}{p(t)^{1+\delta}} = \int rt$$

$$ \int p(t)^{-1-\delta} dp = rt + C $$

Define $C = -rt_c$

$$ \frac{p(t)^{-\delta}}{-\delta} = rt - rt_c $$

$$ p(t)^{-\delta}= -\delta r(t - t_c) $$

Because $t-t_c = -(t_c-t)$ the subtraction inside paren is

$$ p(t)^{-\delta}= \delta r(t_c - t) $$

Define $\alpha = -\frac{1}{\delta}$, take $\alpha$'th power of both sides

$$ (p(t)^{-\delta})^\alpha= (\delta r )^\alpha (t_c - t)^\alpha $$

Let $p(0) = p_0 = (\delta r )^\alpha$

$$ p(t) = p_0 (t_c - t)^\alpha $$

For fitting it is better to use

$$ p(t) = A + B(t_c - t)^z $$

Install lmfit==0.8.3

import pandas as pd, datetime

from pandas_datareader import data

start=datetime.datetime(2001, 1, 1)

end=datetime.datetime(2018, 1, 1)

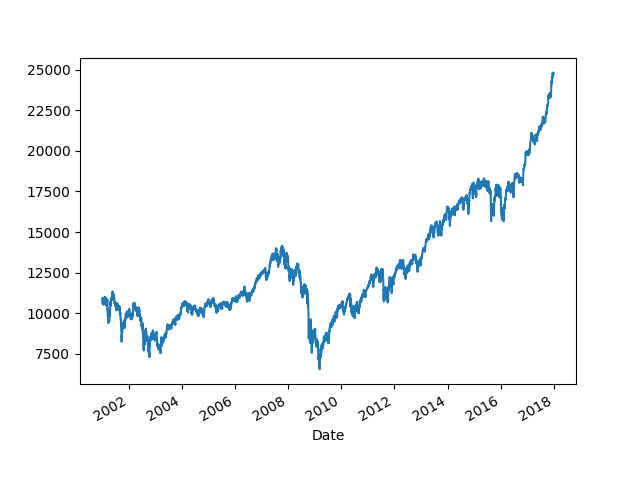

df = data.DataReader('^GSPC', 'yahoo', start, end)

df.to_csv('sp500201702.csv')

df = data.DataReader('^DJI', 'yahoo', start, end)

df.to_csv('dji201702.csv')

import pandas as pd, datetime

#df = pd.read_csv('sp500201702.csv', index_col=0,parse_dates=True)

df = pd.read_csv('dji201702.csv', index_col=0,parse_dates=True)

import pandas as pd

from lmfit import Parameters, minimize

from lmfit.printfuncs import report_fit

def init_fit(min, max, init):

fit_params = Parameters()

fit_params.add('tc', value=init, max=max, min=min)

fit_params.add('A', value=2.0, max=10.0, min=0.1)

fit_params.add('m', value=0.5, max=1.0, min=0.01)

fit_params.add('C', value=0.0, max=2.0, min=-2)

fit_params.add('beta', value=0.5, max=1.0, min=0.1)

fit_params.add('omega', value=20., max=40.0, min=0.1)

fit_params.add('phi', value=np.pi, max=2*np.pi, min=0.1)

return fit_params

def f(pars,x):

tc = pars['tc'].value

A = pars['A'].value

m = pars['m'].value

C = pars['C'].value

beta = pars['beta'].value

omega = pars['omega'].value

phi = pars['phi'].value

tmp1 = (1 + C*np.cos(omega*np.log(tc-x) + phi))

model = A - ((m*((tc-x)**beta))*tmp1)

return model

def residual(pars,y,t):

return y-f(pars,t)

beg_date = df.head(1).index[0].timetuple()

beg_date_dec = beg_date.tm_year + (beg_date.tm_yday / 367.)

end_date = df.tail(1).index[0].timetuple()

end_date_dec = end_date.tm_year + (end_date.tm_yday / 367.)

df['Year'] = np.linspace(beg_date_dec,end_date_dec,len(df))

fit_params = init_fit(2001.0,2100.0,2050.)

y = np.log(df['Adj Close'])

t = df['Year']

out = minimize(residual, fit_params, args=(y,t,))

report_fit(fit_params)

[[Variables]]

tc: 2018.01977 +/- 0.059571 (0.00%) (init= 2050)

A: 10 +/- 0.007098 (0.07%) (init= 2)

m: 0.19663441 +/- 0.019641 (9.99%) (init= 0.5)

C: -0.14243083 +/- 0.007036 (4.94%) (init= 0)

beta: 0.53262341 +/- 0.026568 (4.99%) (init= 0.5)

omega: 13.1485152 +/- 0.151282 (1.15%) (init= 20)

phi: 6.28318530 +/- 0.049456 (0.79%) (init= 3.141593)

[[Correlations]] (unreported correlations are < 0.100)

C(omega, phi) = -0.994

C(m, beta) = -0.993

C(A, m) = 0.972

C(tc, phi) = -0.940

C(A, beta) = -0.940

C(tc, omega) = 0.911

C(A, C) = 0.801

C(m, C) = 0.766

C(C, beta) = -0.729

C(tc, C) = 0.200

C(C, phi) = -0.178

C(tc, A) = 0.173

C(C, omega) = 0.164

C(beta, omega) = 0.147

C(A, phi) = -0.128

C(beta, phi) = -0.121

C(A, omega) = 0.101

Analyze residuals for stationarity, if there, fit was good.

import statsmodels.tsa.stattools as st

res = list(st.adfuller(out.residual,maxlag=1))

print res[0], '%1,%5,%10', res[4]['1%'], res[4]['5%'], res[4]['10%']

-2.90299578531 %1,%5,%10 -3.43196089051 -2.86225180324 -2.56714889993

df['Adj Close'].plot()

plt.savefig('bubble_01.png')